Operational Controls The guardrails that keep GBS honest — and audit-proof.

Controls are not bureaucracy. They are the evidence that your organization can be trusted to handle money, data, and decisions correctly — consistently and without supervision. Understanding them early in your career changes how you read every process you work in.

Sound familiar?

K

KThe four-eyes principleA control requiring that a second, independent person reviews and approves any significant action before it is executed. The most widely applied internal control in GBS finance processes. — why two people are better than one

Four-eyes means an independent second review before significant actions execute. It protects the process — and the person. The model is in THE FIX.

A second pair of eyes

is not about trust.

R

RRavi preps a payment run. Every batch waits for a reviewer.

It feels slow. It feels like being doubted.

Then a reviewer catches a duplicated line in his batch — before it paid out twice.

"That would have had my name on it."

He feels grateful for the control he resented.

You read controls as distrust. They are the reason one mistake stays a mistake.

Three words make the control real — or hollow.

Ravi stops resenting the wait — and starts reviewing others properly. The control is only as strong as the second pair of eyes.

The four-eyes principle in depth

The four-eyes principle is the simplest and most universal internal control in GBS. One person acts. A second person, independent of the first, reviews and approves. Neither can complete the transaction alone.

Performs the action

Creates the payment, posts the entry, sets up the vendor, enters the data. Has full access to prepare but cannot approve their own work.

Independent review

A second person — with no role in the preparation — checks the work against policy, supporting documentation, and approval thresholds. Not a rubber stamp: active scrutiny required.

Approved or rejected

If the reviewer is satisfied: approved, with their ID logged in the system. If not: returned with a reason. Both actions are traceable.

- Payment runs: processor releases invoices for payment → team lead or treasury approves the payment run

- Vendor setup: new vendor created in the ERP → independent review confirms bank details, VAT number, and duplicate check before activation

- Journal entries above threshold: journal posted by analyst → reviewed and approved by senior accountant or controller

- Master data changes: change to payment terms, bank account, or address requires a second sign-off to prevent fraud

- Credit note issuance: credit notes above a defined threshold require approval before release to avoid unauthorized revenue reversal

The most common failure mode for the four-eyes principle is not bypassing it — it is performing it without actually reviewing.

- A reviewer who approves based on trust rather than scrutiny provides no protection.

- Auditors test this by checking whether reviewers can explain what they approved and why.

- A culture where second reviews are rushed or treated as a formality is a culture where controls exist on paper but not in practice.

Four-eyes principle — maker-checker control

Next time you are the second pair of eyes, review as if your name is on it. It is.

Four-eyes is the rule. SoD is the architecture behind it.

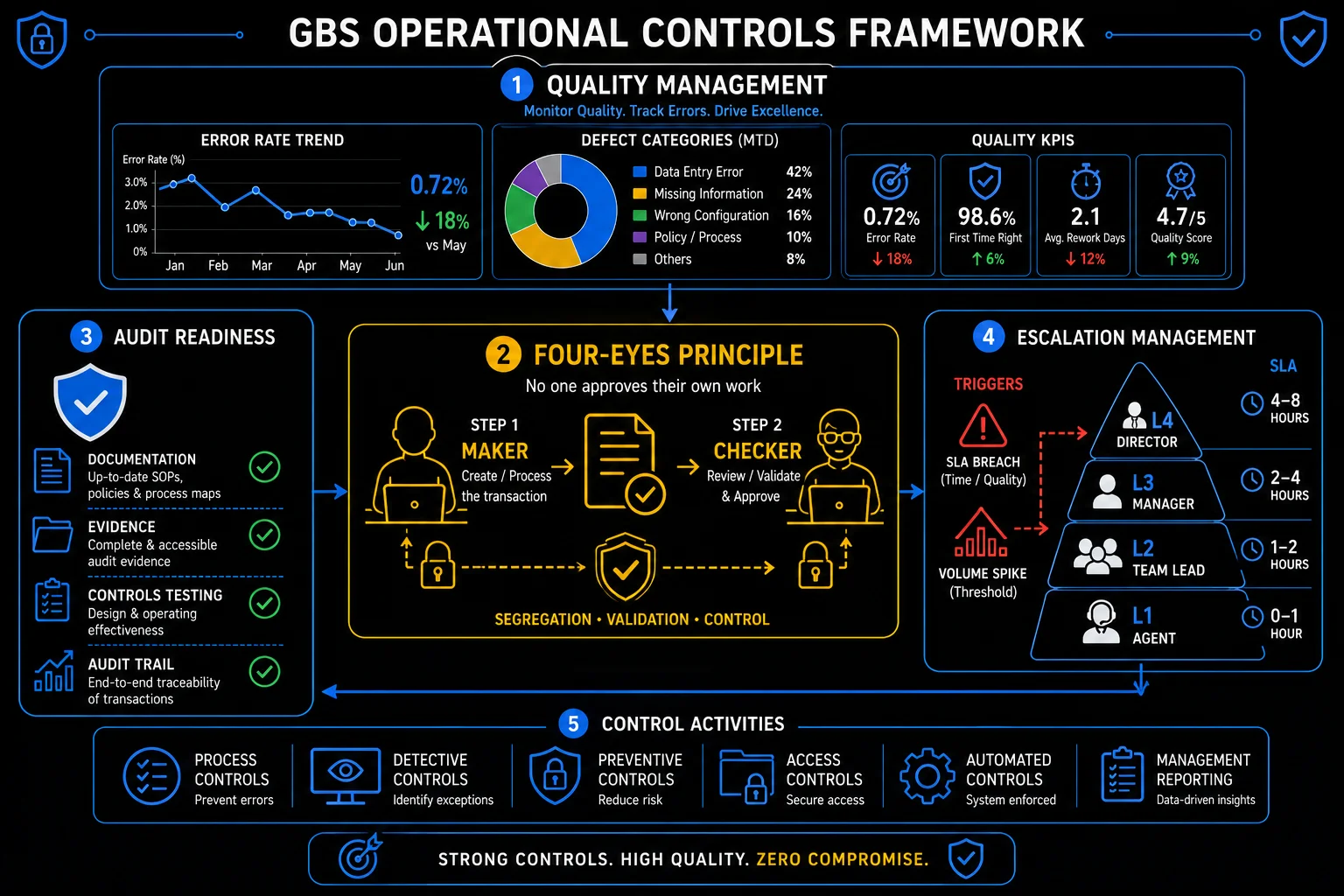

GBS operational controls framework: quality management, four-eyes principle, audit readiness, and escalation tiers

Segregation of dutiesSoD — the principle that no single person should have end-to-end control over a critical financial process. Separating create, approve, and release roles prevents fraud and reduces error risk. — the architecture behind the four-eyes principle

Segregation of Duties: no single person controls a critical process end-to-end. Create, approve, release stay separated. The model is in THE FIX.

You cannot approve your own work.

That rule protects you.

A

AAmara requests system access to cover a colleague’s absence.

Denied: the role would let her both create and approve credit notes.

"But I would never misuse it."

The controls analyst is kind: the rule is not about her. It is about anyone, ever, in that seat. She feels at ease with the no.

You take SoD personally. It is designed for the seat, not the person in it.

Critical processes split into three hands, minimum.

The coverage gap gets solved with a temporary approver instead. The control holds and the work still moves.

Segregation of duties in depth — toxic combinations

If the four-eyes principle is the rule, Segregation of Duties (SoD) is the system design that makes it possible. SoD means that no single person controls a complete financial cycle from start to finish.

- Why it exists: if one person can create a vendor, approve an invoice, and release the payment, there is no check. Fraudulent payments become easy. Errors go undetected for months.

- SOX requirement: for publicly listed companies, Section 404 of SOX requires documented evidence that SoD is designed correctly and operating effectively — tested annually by internal and external auditors

- The most common GBS SoD failure: insufficient headcount. When a small team covers too many roles, individuals end up with conflicting access rights — not by design, but by necessity. Auditors find these and flag them as control deficiencies.

- Compensating controls: when true SoD is not possible (too small a team), a compensating control is required — typically a management review of all transactions performed by the conflicted individual

- System enforcement: ERP access rights (SAP authorization profiles, Oracle role configuration) should enforce SoD at the system level — not rely on policy alone

Check your own access: could you create and approve the same transaction? If yes, flag it. Finding it first counts.

Controls in place daily. That is what audit-ready actually means.

Audit readiness — being "audit ready" every day, not just when auditors arrive

Audit readiness means operating so audits pass as a byproduct — documentation, evidence, and access clean every day. The model is in THE FIX.

Audit season panic

is a choice.

K

KTwo teams, same audit week.

Next door: late nights, reconstructed evidence, screenshots nobody wants to explain.

Klaudia’s team: folders complete, evidence attached at execution time, done by Thursday.

"What did you do differently?" — "Nothing. That is the point."

She feels calm in the one week nobody else is.

You prepare for audits instead of operating audit-ready. The sprint is the failure.

Audit-ready is a daily operating mode, not an annual project.

Audit week costs her team nothing extra — the discipline already paid, in small daily installments.

Audit readiness in depth — the full checklist

The goal is not to pass audits. The goal is to operate in a way that makes passing audits a byproduct of how you normally work — not a sprint you do once a year.

- Control documentation: every key control documented — what it is, who performs it, when, and what evidence it produces

- Evidence of execution: system logs, approval records, review sign-offs — timestamped, traceable, and attached to the transaction or reconciliation they relate to

- SoD compliance: access rights matrix showing who can do what, with no unmitigated conflicts

- Current SOPs: process documentation that reflects how the process actually runs today — version-controlled and recently approved

- Training records: evidence that staff have been trained on current controls — especially after any process or system change

- Exception handling: documented process for what happens when a control fails or an exception occurs — and evidence that exceptions were handled correctly

- Management review evidence: regular review of key reports, reconciliations, and metrics — signed off and dated

- Attach evidence at the time of execution — not six months later when auditors ask.

- Maintain version-controlled documentation that reflects how the process actually runs today.

- Flag exceptions immediately rather than hoping nobody notices.

Quality management — building audit readiness into daily work

Attach evidence to your next control step the moment you perform it. Make it the habit, not the exception.

Even controlled operations have bad Mondays. Here is how the good ones respond.

Handling escalations, volume spikes, and SLA breaches

Spikes, breaches, and escalations are normal operations. Maturity is a response pattern, not an absence of problems. The model is in THE FIX.

Monday: a spike, three escalations.

Your response is your reputation.

M

M8:05 AM. Volume is double normal. A system feed failed overnight.

Two stakeholders escalate before Miguel finishes his coffee.

His instinct: answer every email at once, apologize everywhere.

"Wait — who needs to know what, and when?"

He feels frazzled — and catches himself.

You react to the loudest voice instead of running a response pattern.

Mature teams run the same four moves every time.

By 9:00 one status note reaches every stakeholder. Nobody escalates twice. The spike clears — and his name gains weight, not damage.

Escalations, spikes, and breaches in depth — response levels

In GBS, things go wrong. Systems fail, volumes spike unexpectedly, team members are absent at exactly the wrong time. How you respond to these events defines your operational maturity, and your professional reputation.

- Declare it early: the moment volume is tracking 20%+ above plan, flag it. Do not wait for the backlog to form. Early warning is the single most valuable action.

- Triage the backlog: not all items are equal. Aged items near payment deadlines, items with stakeholder escalations, and regulatory filings have priority over standard aging. Sort and prioritize explicitly.

- Reallocate capacity temporarily: cross-trained team members from adjacent processes can provide surge support for standardized tasks. This is one reason cross-training is a governance requirement, not optional.

- Communicate proactively: stakeholders who find out about a backlog before GBS tells them lose trust permanently. Stakeholders who are told early, with a plan, usually remain constructive.

- Close the loop: after recovery, document what happened, what caused it, and what prevents recurrence. Volume spikes that are not analyzed become recurring surprises.

- Controls are your professional protection, not just the organization's. When something goes wrong in GBS — a payment is made incorrectly, data is lost, a fraud occurs — the question is: was the control in place and was it followed? If yes, you are protected. If not, you are exposed. Following controls carefully, every time, is not compliance theater — it is career risk management.

- The worst escalations are the ones that surprise leadership. An SLA breach that GBS discovered, reported, and had a plan for is manageable. An SLA breach that a business stakeholder raised before GBS leadership knew about it is a trust crisis. The discipline of flagging early — even when you are not certain — is a mark of operational maturity.

- Being audit-ready every day is easier than you think — and harder than most teams manage. The daily habits that create audit readiness (attaching evidence at execution time, version-controlling documents, logging exceptions immediately) take about 5 minutes per transaction. The catch-up sprint to recreate evidence from six months ago takes weeks — and sometimes cannot be done at all.

Escalation framework — structured issue resolution

Write your spike playbook in four lines: assess, communicate, recover, review. Before the next Monday needs it.

The process is protected. Your own day needs the same design.

Key terms in this cluster

Full glossary at the GBS Insider Club Field Guide.

- Exabeam — SOX Controls: Common Types, Examples & Implementation Practices

- SecureEnds — Segregation of Duties in Internal Controls: Framework and Best Practices

- Ramp — Segregation of Duties in Accounts Payable Explained

- Zampa Partners — The Four Eyes Principle in Sanctions Monitoring: An Internal Audit Perspective

- SafePaaS — Why Segregation of Duties is Critical for SOX Controls

- Pathlock — Internal Controls for SOX Compliance: A Practical Guide

- ACFE — Association of Certified Fraud Examiners, 2024 Report to the Nations: SoD fraud detection statistics

- ✓ Four-eyes principle — the most universal GBS control, with examples

- ✓ Segregation of Duties — design principles, SOX requirements, ERP enforcement

- ✓ Audit readiness — daily habits that make audit prep a formality

- ✓ Escalation matrix — L1/L2/L3 escalation triggers and response frameworks

- → Personal Productivity — Eisenhower Matrix, time blocking, inbox zero — Cluster 5

Want the full breakdown on video?

GBS operational controls covered in depth on the GBS Insider Club YouTube channel.

▶ Subscribe on YouTubeKnowing the frameworks is the entry ticket. Applying them — visibly, at your actual job — is what gets you promoted.

The GBS Insider Club Career Playbooks turn this theory into a guided 90-day program for your role: self-assessment, practical exercises, templates, and Julian's unfiltered practitioner playbook.

Explore the Career Playbooks → Back to Operational Excellence