Value Creation and Commercial Logic GBS delivers more than cost reduction. Most of it goes uncredited.

Cost reduction gets the business case approved. Everything else is what makes GBS genuinely strategic — and almost none of it appears in a P&L line.

Sound familiar?

R

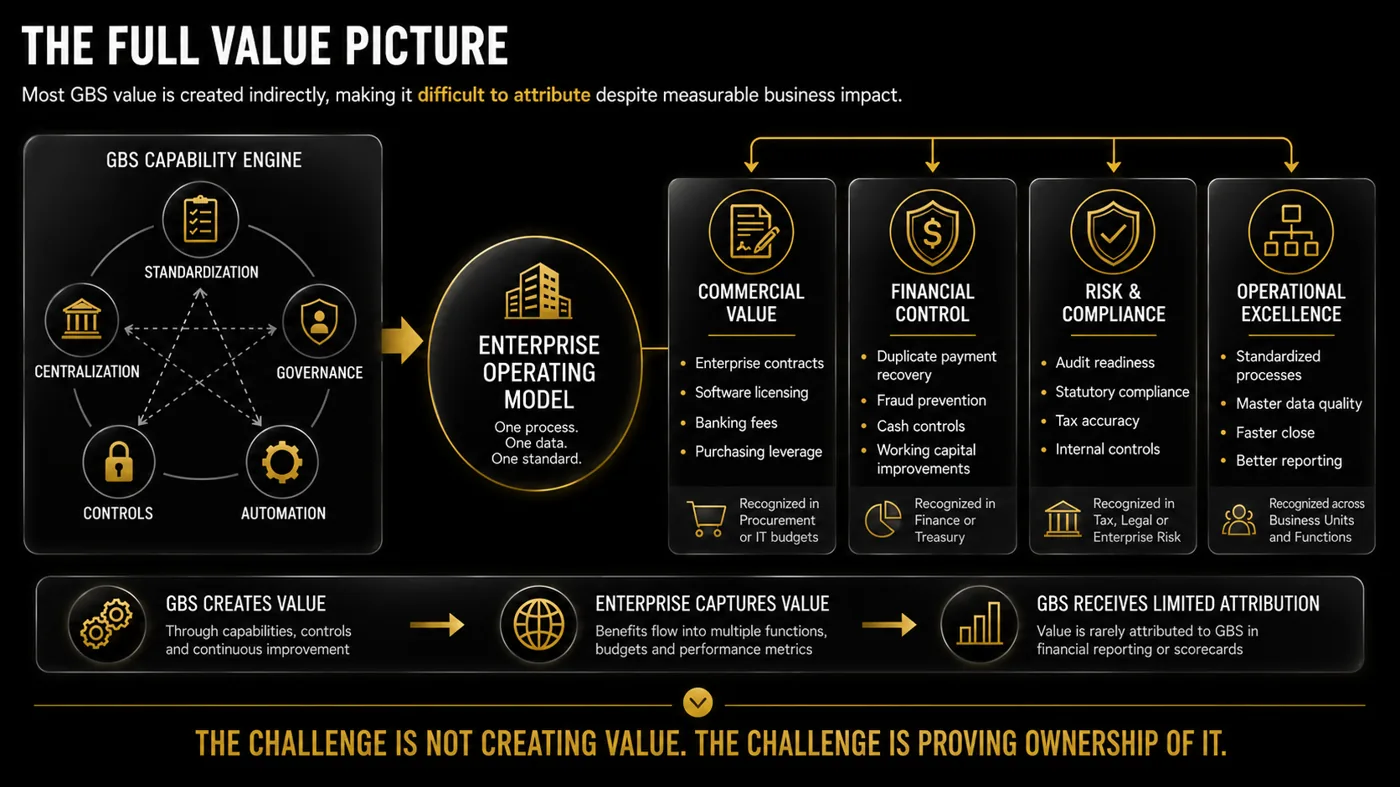

RThe full value picture

GBS creates hard and soft value far beyond headcount savings. Most of it never gets attributed. The model is in THE FIX.

Your work saves money.

The report calls you a cost.

R

RBudget season. A townhall slide shows Ravi’s team as one line: cost.

Last month his team caught duplicate vendor payments before they left the bank.

Nobody counted that anywhere.

"If we only cost money, why are we here?"

He knows the answer exists. He just cannot point at it. He feels invisible.

You deliver value every week and report only cost. The organization believes what gets reported.

The value is real — it needs names. Hard value gets measured. Soft value gets argued.

Ravi adds one prevented-error line to his monthly update. The next deck still says cost — but his team lead now has an answer ready.

The full value picture — hard and soft value in depth

The 41% figure is not evidence that GBS fails to create value. It is evidence that GBS fails to capture and communicate the value it creates.

Technology vendors, software providers, and professional services firms price differently when negotiating with ten country entities versus one central team.

- Volume leverage reduces unit cost before a single process is touched

- ERP licenses, audit fees, banking fees — all compress at scale

- Savings are real but rarely traced back to the GBS team that created them

APAccounts Payable — the process of managing, validating, and paying supplier invoices centralization almost always surfaces duplicate payments — some dating back years before the transition.

- Recoverable amounts are rarely trivial

- Pre-transition duplicates surface during AP normalization

- Requires systematic matching logic — a natural GBS process control

Standardized processes and documented controls reduce the risk of missed deadlines, late filings, and regulatory breaches.

- The cost of a penalty never incurred does not appear in any savings report

- Transfer pricing consistency improves when one team owns the process

- Statutory deadlines managed centrally have lower miss rates

External auditors work faster and at lower cost when processes are documented, consistent, and operated by a single team with clear controls.

- Audit preparation time drops significantly post-centralization

- Control deficiencies reduce — one team, one standard, one audit trail

- Balance sheets and P&L are cleaner when postings follow standardized rules

The full value picture — GBS creates the value, the enterprise captures it. The challenge is not creating value; it is proving ownership of it.

Cost levers — headcount, real estate, vendor consolidation

When ten country teams run the same process differently across different system configurations, an ERPEnterprise Resource Planning — integrated platform managing finance, HR, procurement, and supply chain across the organization upgrade is a multi-year program.

- One GBS running a standardized process means a controlled rollout

- Testing scope, data migration, and training all compress significantly

- The upgrade cost difference between fragmented and centralized delivery is substantial — and almost never attributed to GBS

Vendor records, customer data, cost centers, material codes. When scattered across entities, nobody owns them. When centralized, governance becomes possible.

- Data ownership fragmentation is the norm — procurement, finance, and operations each own part of a vendor record, none own all of it

- Centralization does not automatically fix MDM — but it makes fixing it possible

- The downstream value: fewer errors, faster processing, more reliable reporting

Before centralization, process knowledge lives in individuals. It is siloed, fragmented, undocumented, and outdated.

- A functioning GBS makes knowledge explicit, transferable, and auditable

- When someone leaves a fragmented operation, the process often leaves with them

- Documented SOPsStandard Operating Procedures — written documentation of how a process should be executed, including steps, inputs, and expected outputs and DTPsDesktop Training Procedures — step-by-step task-level documentation, more granular than an SOP are institutional resilience — the value is invisible until you need them

When the GBS produces consistent, timely, and accurate data, leadership makes better decisions. That causal link is real — and almost impossible to attribute.

- Consolidated reporting replaces fragmented country spreadsheets

- Insights shared with business leaders are only possible when someone owns the data

- 52% of organizations are already moving GBS toward decision support and business partnering (SSON, 2026)

A well-run GBS is one of the best sources of future finance and operations leaders. Associates who rotate through multiple processes, geographies, and functions build breadth that is rare in functional silos.

- Cross-functional exposure at scale is a GBS structural advantage — not available in country-level roles

- Organizations that treat GBS as a leadership development engine see measurable retention and promotion rates above average

- This pipeline value never appears in the business case. It should.

Value drivers — insights, process intelligence, advisory, automation

Only 41% of companies believe their shared services create tangible value (BCG, 2024). The value exists. Most of it just never gets traced back to a P&L line.

- The GBS does not get credit for the audit that went smoothly, the ERP upgrade that stayed on schedule, or the duplicate payment recovered three years after transition.

- It gets measured on cost per FTEFull-Time Equivalent — unit measuring workforce capacity. 1.0 FTE equals one full-time employee working standard hours. and SLAService Level Agreement — contractual performance standard defining response time, accuracy, and availability. attainment, then asked why it is not a strategic partner.

Data monetization in GBS is discussed more than it is practiced. The structural reason: most business data has no single owner.

- A vendor master record is needed by procurement (sourcing), finance (payment fields), and the business (product delivery context). Each party owns part of it. Nobody owns all of it.

- The same fragmentation applies to customer records, product data, and fixed assets — each touched by multiple functions with different data needs.

- Until master data ownership is resolved, monetization remains theoretical.

- The practical value of good data in GBS is not in selling it — it is in making it accurate, consistent, and usable for the business that already owns it. That is where the real return is.

Add one prevented-error or saved-hour line to your next status update. Name the value, even small.

Value has names now. Costs need honest ones too. Meet TCO.

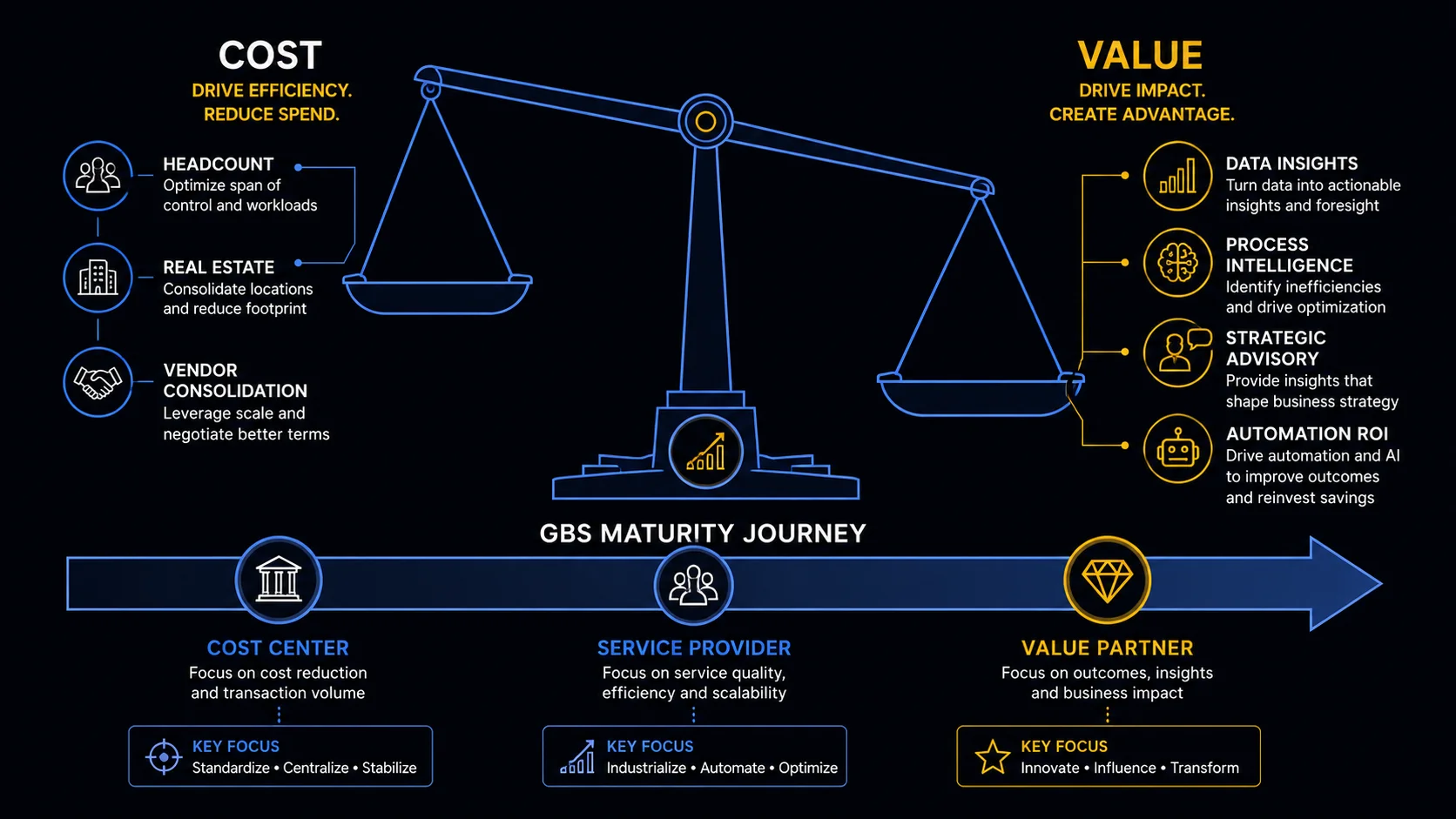

From Cost Center to Value Partner — the GBS maturity journey

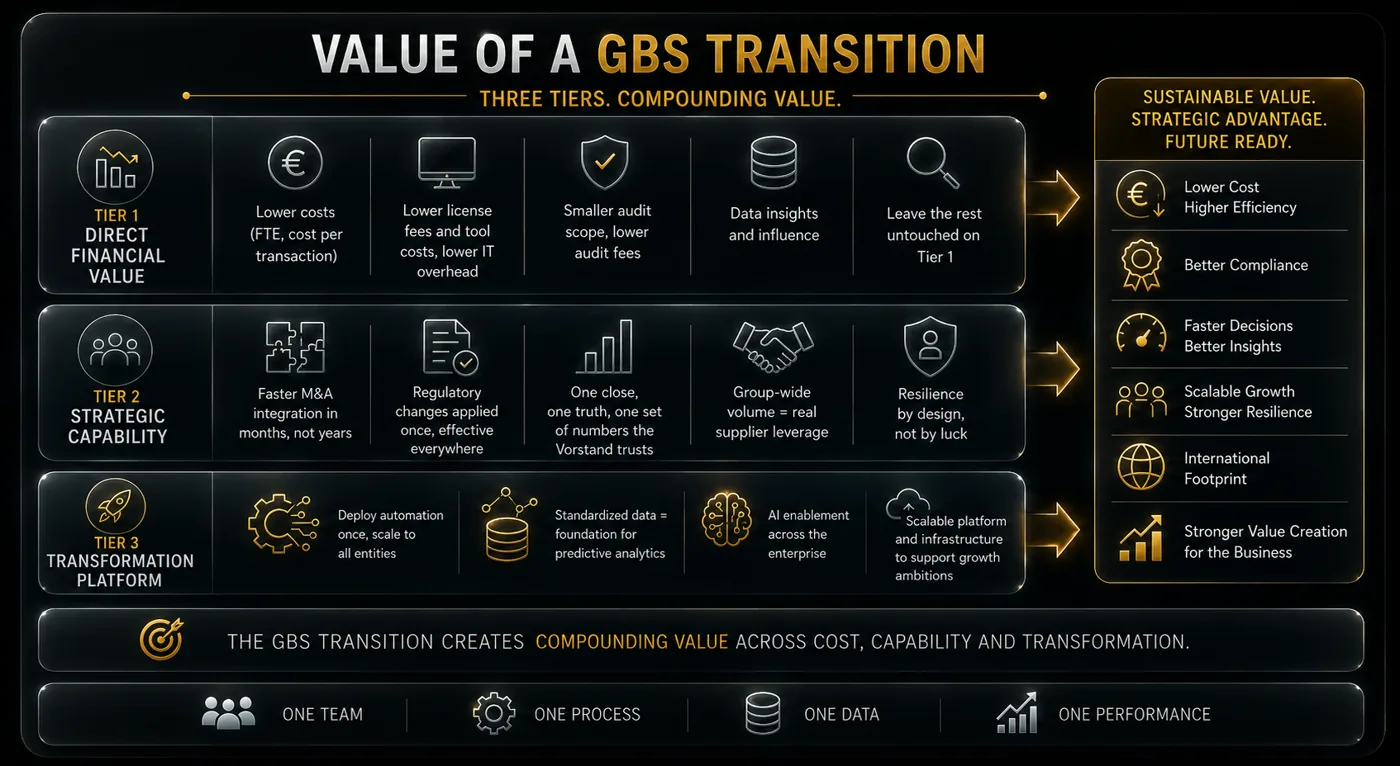

The value of a GBS transition goes well beyond labor arbitrage — cost, capability, and transformation compound over time

TCOTotal Cost of Ownership — the full cost of delivering a service, including direct and indirect costs, not just visible headcount. and Cost-to-Serve — how costs are actually measured

TCO counts everything — direct, indirect, hidden. Cost-to-Serve prices it per transaction. Both decide how cheap your team really is. The model is in THE FIX.

Your team looks cheap.

Until someone counts everything.

P

PA consultant deck lands. Peter’s cost per FTE looks great.

Then the CFO asks one question.

"Is that with IT, facilities, and management overhead — or without?"

Peter checks. Without.

The honest number is a third higher. He feels cornered.

You quote the visible cost. Decisions get made on the full one.

TCO is a discipline about what you include.

Peter re-baselines with full TCO before anyone asks again. The next review holds no surprise question.

TCO and Cost-to-Serve in depth — full cost structures

Most GBS business cases compare total cost before centralization to total cost after. That is TCO done correctly. The discipline is in what you include.

A TCO comparison that only captures the visible costs will overstate the business case. The missed items above typically add 15–25% to the real cost on both sides of the comparison.

Source: Gartner, Five Shared Services Pricing Approaches. Neither model is universally correct — the right choice depends on organizational maturity and what behavior the business wants to incentivize.

Ask what your team’s fully loaded cost per FTE includes. Learn which lines are missing.

Costs counted honestly. Now the two numbers that decide funding. Payback and ROI.

The financial case — payback and ROI

Two numbers carry every GBS business case: payback period and ROI. Ideas without them stay ideas. The model is in THE FIX.

Good idea. No number.

No decision.

K

KKlaudia pitches an automation idea in a team meeting.

Heads nod. Nothing happens.

Six weeks later she asks her manager why.

"Nobody could say when it pays for itself."

The idea was good. The case was missing. She feels dismissed.

You sell the idea and skip the math. Leadership funds math.

Two numbers carry the case. Both fit on one line.

She reframes: one-time effort, hours saved per month, payback in months. The same idea gets a scoping call.

The financial case in depth — payback, ROI, and the wider value

A GBS set-up has to be justified financially. Two KPIs carry the business case: payback period and return on investment. The wider value is harder to put in a single number, but it is often what makes the case attractive.

How long until the total investment pays for itself. The primary decision gate for most GBS programs.

One client analysis found the payback period for building a captive center was more than double that of outsourcing — over four years versus under two (Auxis/Deloitte, 2024). The model choice affects the payback math significantly.

A CFO approving a multi-year transition wants to know when the organization crosses into positive cash territory — not the theoretical run-rate saving in year five.

Total value generated divided by total investment. What you count as value decides whether the number holds up.

Run-rate savings are projections. P&L-realized savings are what finance will accept. The gap between the two is where most business cases lose CFO confidence.

A business case built entirely on soft savings will not survive scrutiny. One that ignores them undervalues the program. Put each benefit in the right category and do not overstate it.

- Headcount reduction and redeployment

- Contract and license consolidation

- System decommissioning

- Duplicate payment recovery

- Facility and infrastructure cost reduction

- Capacity release (same headcount, more output)

- Avoided penalties and compliance costs

- Audit cost reduction

- Error rate reduction and rework avoidance

- Faster ERP upgrade execution

The value can be lost as easily as it is built — eight risks that erode it, and how to mitigate each

Take your best improvement idea. Estimate effort once, savings per month. Divide. That is your payback line.

The center proves value with numbers. You prove yours differently.

- Cost reduction is the entry ticket, not the destination. The organizations that extract genuine value from GBS are the ones that measure what the model makes possible — not just what it costs less.

- The value that goes uncaptured is not invisible — it is just not on anyone's reporting template. Audit quality, ERP upgrade speed, data governance — these are measurable with the right tracking discipline.

- The business case conversation with a CFO is won on payback period and realized savings, not on a list of strategic benefits. Build the financial case first. The narrative follows.

- Most GBS organizations are sitting on a talent pipeline story they have never told. Associates who move through multiple processes and geographies become your best future finance and operations leaders. That story is free to tell and almost never told.

The GBS maturity journey — cost center to value partner

What this means for your career

Two things beat technical skill early on: business understanding and value framing. The model is in THE FIX.

You know your process cold.

The business, not at all.

R

RRavi can run his queue blind.

A stakeholder asks what the business unit he supports actually sells.

He does not know.

"You process our invoices — and you don’t know what we make?"

The gap stings. He feels small.

Process mastery gets you kept. Business understanding gets you asked for more.

Two habits separate associates who grow fast, and neither is technical.

Ravi spends one lunch a week reading about his business unit. His questions in calls change first. Then the way people answer him.

Career implications in depth

Two things matter more than technical competence in the first two years of a GBS career.

- Most GBS associates know their process well. Far fewer understand the business they are supporting. That gap is the career differentiator.

- Learn what your business unit actually does to generate revenue — what they sell, who they sell it to, what slows them down

- Understand what administrative burden your process creates for the business — approvals required, data requests, exceptions, rework loops

- The less burden you create, the more the business can focus on selling and producing. That connection is the definition of GBS value.

- Ask questions that go beyond your transaction. "Why does this approval exist?" is a career question, not just a process question.

- GBS organizations regularly keep themselves busy with work that has no clear value for anyone — requirements assumed, approval thresholds unchallenged, reports produced because they always have been

- Every approval, every report, every workflow step should have a named beneficiary and a clear purpose

- If you cannot identify who benefits from a process step and how, that is a question worth raising — tactfully, with evidence, not as a complaint

- The business wants less friction, better data, and fewer hurdles — not more controls nobody asked for

- Associates who understand the business well enough to identify what is slowing it down — and have the credibility to suggest change — build careers faster than those who only execute

Knowing what to change is step one. Knowing how to raise it without damaging the relationship is step two. Stakeholder communication and career positioning — how to build credibility, frame improvement ideas, and navigate organizational dynamics — are covered in Pillar 4 (Stakeholder and Communication) and Pillar 5 (Career and Performance).

Find out what your supported business unit sells and to whom. One page, one lunch break.

You can name your value. Next: who actually runs the place. Cluster 3: Structure & Governance.

Key terms in this cluster

Additional terms used in this cluster. Full cross-pillar glossary available at the GBS Insider Club Field Guide.

The GBS maturity journey — cost center to value partner

Want the full breakdown on video?

Value creation, business case metrics, and the CFO conversation — covered in depth on the GBS Insider Club YouTube channel.

▶ Subscribe on YouTubeKnowing the frameworks is the entry ticket. Applying them — visibly, at your actual job — is what gets you promoted.

The GBS Insider Club Career Playbooks turn this theory into a guided 90-day program for your role: self-assessment, practical exercises, templates, and Julian's unfiltered practitioner playbook.

Explore the Career Playbooks → Back to GBS Fundamentals